Security as a Service: Has the “App Store Moment” for OEMs in Europe Arrived?

TL;DR

Tesla’s Q4 FY25 earnings highlight a pivotal shift in automotive economics: software subscriptions are emerging as a major high-margin growth engine alongside vehicle sales. Much like the platform transformation triggered by the iPhone and the launch of the App Store, the modern software-defined vehicle is evolving into a recurring-revenue ecosystem built on digital services. In Europe, where consumers demand clear value, Security as a Service subscriptions can unlock sustained post-sale revenue from the installed fleet, while addressing growing consumer demand for protection and value.

For years, the debate has raged: Is Tesla an automaker or a tech company? The recent release of Tesla’s Q4 FY25 earnings (ended January 2026) provides the strongest evidence yet that the transition to a tech-first business model is accelerating.

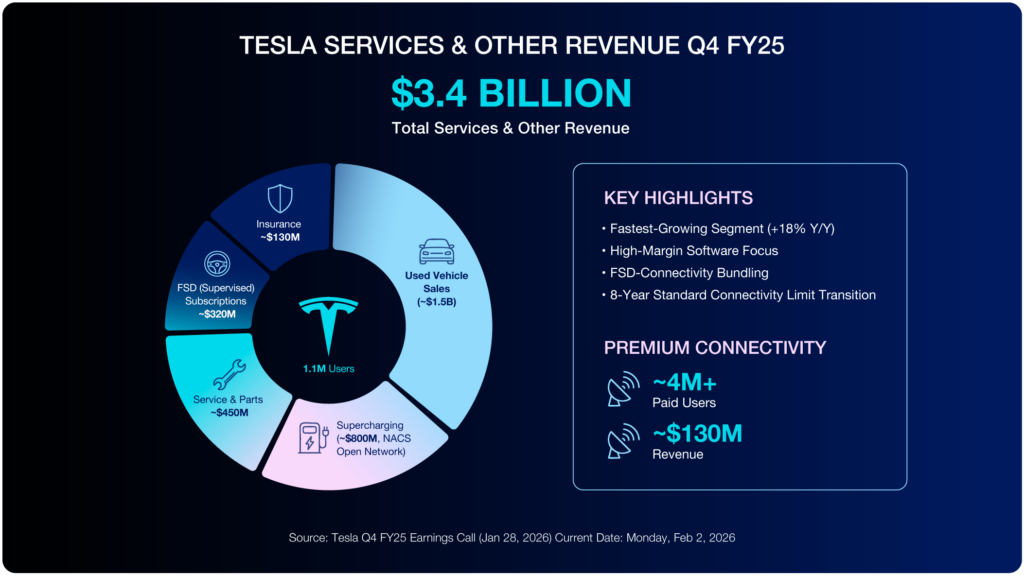

While the headline revenues of $24.9 billion is significant, the real story – and the future of automotive profitability – lies in a smaller, yet rapidly expanding slice of the pie: the $3.4 Billion generated by “Services & Other.”

As the image below illustrates, this segment is no longer just about fixing cars; it’s about monetizing the existing fleet through high-margin software.

Hidden Margin Engine

The Q4 FY25 earnings data shows that “Services & Other” grew by 18% year-over-year, making it Tesla’s fastest-growing segment.

To understand the significance of this trend, it’s important to examine the composition of that $3.4 billion. While it includes lower-margin, necessary businesses like selling used trade-ins (~$1.5B) and physical parts, the star performers are digital.

Based on Tesla data, if we combine FSD (Supervised) Subscriptions (~$320M) and Premium Connectivity (~$130M), we are seeing nearly half a billion dollars in quarterly revenue derived almost entirely from high-margin software.

Unlike manufacturing a Model Y, which involves massive capital expenditure, supply chains, and labor, scaling a software service to the current 4M+ paid connectivity users costs comparatively little. And this aligns with the holy grail of modern tech business – recurring SaaS revenue.

The Apple Paradigm: From Hardware to Ecosystem

We’ve seen this movie before.

In 2007, Apple launched the iPhone. It was a revolutionary piece of hardware. But the real business revolution didn’t happen until 2008 with the launch of the App Store. Suddenly, the iPhone wasn’t just a product you bought once; it was a platform you paid into continuously. Apple shifted from relying solely on cyclical hardware upgrades to building an impregnable fortress of services revenue (iCloud, Apple Music, Arcade).

Tesla is currently executing its own “App Store moment.” The car is the hardware platform. Premium Connectivity ($9.99/month for satellite maps, live traffic, and streaming data) is the gateway service, much like iCloud storage. FSD subscriptions are the premium-tier specialized app.

In the US, the cultural acceptance of subscription models is deeply embedded, making this transition relatively smooth. But what about other markets?

European Dynamic: Skepticism vs. Value

The European market has historically been more skeptical of “subscription creep” than the US. European consumers are value-conscious regarding recurring payments and benefit from stronger regulatory protections against drip pricing.

However, the narrative that Europe “won’t pay for subscriptions” is false. Europe will pay, but the value proposition must be undeniable. We saw this with the eventual embrace of Spotify and Netflix, once their utility became indispensable.

For Tesla to replicate its US software success in Europe, the hook might need to be different. While streaming Netflix in the car is “nice to have”, streaming data for security is a “must-have.”

Security as a Service: The Ultimate European Value Proposition

The automotive threat landscape is evolving rapidly. We are moving past simple window-smashing and hotwiring into an era of sophisticated keyless theft techniques and potential cyber threats against connected vehicles.

This is where Tesla’s software model can shine in Europe.

Imagine a “Premium Security Shield” subscription focused on the type of on-board cyber protection pioneered by firms like PlaxidityX. This layer wouldn’t rely on a cellular signal; it would operate at the “edge,” deep within the vehicle’s central compute platform.

Instead of just recording a theft in progress, this software would actively monitor internal vehicle networks (e.g., Ethernet or CAN bus) for anomalous behavior typical of advanced hacking attempts or key fob spoofing. It could identify and block unauthorized commands instantly—even if the car is parked three levels underground without a network connection.

In a European market highly sensitive to asset protection and rising insurance costs, a monthly subscription that actively hardens the vehicle against sophisticated offline attacks offers undeniable value. It transforms a subscription from an avoidable entertainment cost into a necessary defensive shield.

Outlook for 2026

Looking at Tesla’s Q4 FY25 data, it’s clear that the “software-defined vehicle” is no longer a buzzword – it’s a verifiable, high-growth P&L line item.

As we move deeper into 2026, the metric to watch isn’t just how many cars Tesla delivers. We should also pay attention to how effectively they monetize their nearly 9 million-strong installed base by offering subscription services—whether entertainment or security—that car owners decide they cannot live without.

Published: March 30th, 2026